Interview with Anne-Sophie DELATTRE, IGL / Project Manager, Crédit Agricole SA

and Eva HÖGLUND, Chief Financial Officer, EFL Crédit Agricole Group

Produced by: Mireille de Kerleau, Communications Manager, CACEIS

With the intervention of Mamadou FALL, General Director of Kossam

and Marie FAYE, Administrative and Financial Director of Kossam

Hello, for the fourth edition of this podcast dedicated to Solidarity Bankers, I invite you to board a ferry that connects Dakar to Gorée Island, in Senegal.

Eva : It was during a weekend, when we visited Gorée Island, there were lots of children, and they were singing during the ferry crossing, and it was quite nice, so I filmed them.

Eva Hoglund is speaking to us. In this podcast, we'll discover her journey as a Solidarity Banker, alongside Anne-Sophie Delattre.

You're going to tell me, what are they? Solidarity Bankers Well, Solidarity Bankers is a skills-based volunteer program. It's open to all Crédit Agricole Group employees, and it involves missions supporting microfinance institutions and impactful businesses, supported by the Grameen Crédit Agricole Foundation.

So before I begin, I'll just remind you that Senegal is a predominantly rural country. Livestock farming represents 7.5% of the national GDP and 35% of agricultural GDP, but Senegal depends heavily on the importation of milk powder: 90% of the milk consumed in Senegal is imported in powder form, while 30% of the population traditionally lives from livestock farming and can produce this milk. It was in response to this observation that Bagoré Bathily created a social enterprise in 2006 called The Shepherd's Dairy, with the aim of promoting local dairy production. Today, La Laiterie is the leading national company processing local milk. Its subsidiary, called Kossam, is responsible for supervising and improving milk production and collection systems.

So there you have it, the scene is set, I suggest you now discover who Eva and Anne-Sophie are.

Anne-Sophie : My name is Anne-Sophie Delattre and I have been with the Crédit Agricole group since the end of 2006. First, with an initial experience of more than 10 years in the Crédit Agricole Consumer Finance subsidiary, and a final experience at CACF while expatriating in China where I was responsible for Risks and Permanent Controls for 4 years. And then following this experience in China, I returned to France, to the headquarters of Crédit Agricole SA and I work in the Group General Inspection, I am a project manager at the international retail banking division. This is what I have been doing since my return from China, so in April 2018.

Eva : My name is Eva Höglund. I joined the group in 2001, first at CACF, where I worked in the international department as a supervisor for various CACF subsidiaries abroad. In 2010, I left for my first expatriation to Denmark, and then I continued with a second expatriation to China, and that's where I worked day-to-day with Anne-Sophie. Anne-Sophie was responsible for risks, and I was responsible for finance. Then, when I returned from China, I joined BPI, Banque de Proximité à l'International, at the headquarters in Paris. And for two years now, I've been an expatriate again, in the financial department of EFL, the leasing and factoring entity in Poland.

So, you're Polish, Eva.

Eva : No, I'm Swedish

Ah Swedish, not Polish at all, okay.

Eva: Nothing to do with it, I don't understand a word!

So Anne-Sophie and Eva knew each other from having worked together a few years earlier as expats in China. I asked Eva how they learned about the Solidarity Bankers mission and how they ended up together in Senegal.

Eva : There you go... actually, I had already done a Solidarity Bankers mission, it was in 2019 I think, and I had been to Kenya. I had great memories of it, it went very well, it was also very rewarding because the company really used what I had proposed. And when I saw this offer, I saw that it was in finance, I saw that it was still in Africa, that interested me, and I saw ideally, a Risks and Finance duo. I said to myself, there you go, Anne-Sophie, she's adventurous like me, I sent her a message right away, and she replied right away. I said to her: but are you sure? Because if we apply, I'm sure we'll get it. Because, really, our complementarity was perfect for what the ad said, and I said to myself, but no two others are going to have the same proposal. And we got it.

Next, I asked them to tell me about the social enterprise they've been supporting over the past two weeks in Senegal. Anne-Sophie begins by telling us about Kossam.

Anne-Sophie : It's a company whose main mission is a social one. La Laiterie du Berger is a company with a capitalistic mission, you could say, to make a profit, which isn't necessarily the case with Kossam; that's really what makes it special. Kossam today, well of course, the interest, seeks balance in its activities, but it is very strongly tinged by the social mission of developing the milk collection subsidiary in the north of Senegal in fact, since the CEO of Laiterie du Berger, in fact, when he set up this company, it was following an observation that cattle are used only for meat and that milk, ultimately, we did nothing with it in Senegal, and so he said to himself we cannot let this material go to waste, not be exploited so Laiterie du Berger makes yogurts and Kossam develops the entire collection structure and as a result, aims to improve the living conditions of breeders, to develop female employment since 53% of breeders are female breeders today. And they also have a farm school in which they support women, breeders, or farmers to optimize milk production, help them to properly care for their animals and incidentally also try to teach them some methods for growing vegetables for example that they can implement in the villages when they return later. So it was really a very different prism, for us who are bankers at the base, to say to ourselves, in fact, each activity is not seen through a prism of profitability but more through a prism of social impact.

And Eva summarizes the overall structure for us.

Eva Kossam is a subsidiary of Laiterie du Berger. It was created by Laiterie du Berger, which owned 100% of it until last year, when they brought in the cooperatives, the livestock farmers' cooperative. Today, Laiterie is the main shareholder, at 95%, and the cooperative owns 5% of Kossam.

So why did Kossam call on Solidarity Bankers? Mamadou Fall, Kossam's CEO, spoke to Anne-Sophie.

Mamadou Fall : The maturity phase that Kossam is now entering requires a good command of operational processes, effective financial monitoring and ongoing risk monitoring. The quality of work and the pragmatism of the solutions proposed by the Solidarity Bankers missions from which we have already benefited motivated us to source this new mission to help us structure these issues.

I then wanted to know more about their missions themselves: what their objectives were, how they went about it, and with which company stakeholders.

Anne-Sophie : we had 3 projects: a project that Eva and I tackled together, which was Organization and Processes, a project more on Financial Reporting which was led by Eva and a Risk Mapping part on which I was more in charge on my side.

So on the Organization and Processes part, we worked based on interviews with the Executive Committee. So there, the principle was to discuss with them and understand the company's major processes, to have them explain to us the detailed functioning of their processes, what could be the blocking points or the risks that they already had in mind, the areas for improvement that were already underway. So, we already discussed all that a little and then, on the basis of these interviews, afterwards, with Eva, we established observations, a diagnosis and recommendations that we then shared within the framework of the Steering Committee that we had every two days. So we really built everything with them, shared the action plans, and validated the rest to be done with them. And then after, on the Risk Mapping part, we still started with quite a few interviews and also observations from Eva's project on Financial Reporting. So here it was rather me who built a risk-based approach to set up a management system, or at least a control system by identifying advanced operational risk indicators, and that, in this case, it was me who built it and I was the one who shared it with them afterwards. So here, we are rather in a stage where they must appropriate the tools that were transmitted at the end of the mission and we remain available to discuss with them and finalize them.

Anne-Sophie's response raised a question in me: what types of risks might the company face?

Anne-Sophie : Unsurprisingly, we have a major operational risk, which then breaks down into sub-themes of risks. The operational risk is very critical because it relies on key people, and on a process context in a company, in a country subject to fairly high climatic risks, water shortages, processes that are very manual and basically, the collection is done by tricycle drivers, in the bush. A tricycle accident seems silly, but we are really dealing with a first-level risk. If there is a tricycle accident, the collection does not reach the Dairy, so the farmers do not earn their money, it is a net loss for everyone. These are the risks linked to operations and then after, at the Kossam level, I think you will confirm Eva, we have a key person risk, which is very very high since we have no backup on the Management Committee and we have roughly 4/5 people who are really key in the company. Then there are slightly more detailed risks: tax risk, financial risk, and things like that, but it's a little less glaring, I'd say, than operational risk and key-person risk. Eva, do you want to talk about your work on the reporting side? Because it's still a major pillar of the mission?

Eva : Anne-Sophie quickly mentioned the tax risk, which is due to the fact that there is no transfer pricing in place, which is a fairly significant risk because there are many activities that link Laiterie du Berger and Kossam, but without a transfer premium between the two. This creates a significant tax risk. And then, the financial risk that Anne-Sophie mentioned is a fairly basic risk since it is not an interest rate risk or an exchange rate risk or a liquidity risk, it is really a financial reporting risk since everything is manual. It is linked on the one hand to the key person. If the key person is not there for the reporting, it will not be done. And then, because everything is manual, it also creates a fairly high risk of error. And then we also worked on the target financial reporting. The current reporting was a bit too simple and complicated at the same time: it repeated the same data from one page to the next, and it wasn't necessarily the same figure from one page to the next. And we identified the new target reporting with them. And now, based on the presentation proposal I made to them, I'm waiting for them to verify it and confirm it. So the ball is now in their court; we remain available to work with them post-mission until the end of June. And now we remain available if they need us.

Marie Faye is Kossam's Administrative and Financial Director. She tells us about the contribution of the Solidarity Bankers mission to her daily work.

Marie Faye : I expected the mission to serve to strengthen administrative improvement capabilities – I am the administrative and financial director of Kossam. And today, at the end of your mission, I admit that it will change a lot in our daily work. For example, I can cite, it will allow us to minimize risks, to strengthen our financial productions such as reporting and at the same time to save time mainly, I will be able to move from operational tasks to more strategic tasks.

To conclude, I wanted to know what our two bankers had gained from their mission.

Eva : do you want to start Anne-Sophie?

Anne-Sophie : I was going to tell you, come on, I'll go for it. Yes, it was very interesting, in fact, this whole social dimension, I hadn't necessarily taken it into account before leaving, in fact, I hadn't really integrated it. And so, it's still super-interesting and super-rewarding to think that we're working to ultimately help develop villages, to increase the standard of living of a population through the profitability of milk collection, through securing processes and other things. And then, being confronted with operational processes in the bush, that was also very interesting, you'll tell me what you think, Eva, but overall, in hindsight, I tell myself that it was really funny to find ourselves, one morning like that, at the collection, at 7 a.m. with the collector arriving with his son on his tricycle and his cans, the breeders arriving with their cans, their buckets of milk to register the morning's milking. And then, the second observation that I will also make is that ultimately, I started with a lot of certainty about what I was going to deliver at the end of this mission and I did not at all deliver what I had in mind because we had to put ourselves back in a small entity context, with few people and we are often used to bringing out the heavy artillery and there, we had to be very operational, so reframe the deliverables a little with regard to the whole risk mapping part. So that was what was quite interesting because we had to rebuild tools, rethink things on site, and deliver things that perhaps seem a little easy from our point of view, but which I think will greatly help them.

Eva : I find that these solidarity banker missions are truly unique experiences, and I think we're very lucky to be in a group like Crédit Agricole where we have the opportunity to participate in such missions. It really requires a significant open-mindedness, because you have to adapt to an activity that isn't ours. Neither Anne-Sophie nor I are dairy farmers or cow breeders. We're experts in finance and risk, but in financial institutions. So you really have to adapt to the size of the company, to the company's activity, and in a context that isn't ours at all. For me, it remains one of the best memories, seeing this sandy landscape, women who came from here and there, from a house, they sometimes came from quite far away, in fact, on foot. And who came to drop off these two liters of milk in these colorful clothes, very often with the children who accompanied them, and that was a beautiful experience that I feel very lucky to have been able to experience.

A very satisfying mission for our two solidarity bankers. I hope this testimony has inspired some vocations among our listeners and I look forward to seeing you for the next episode of Solidarity Bankers… see you soon!

Listen to the podcast here

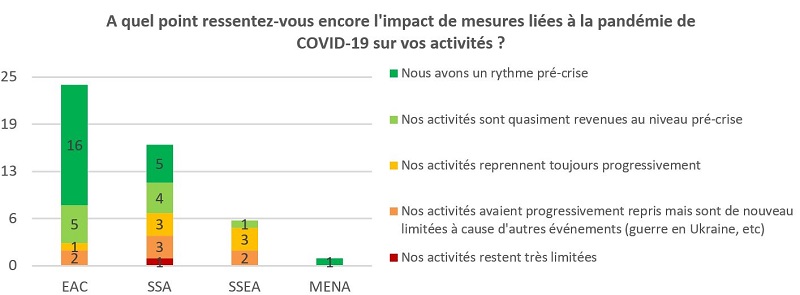

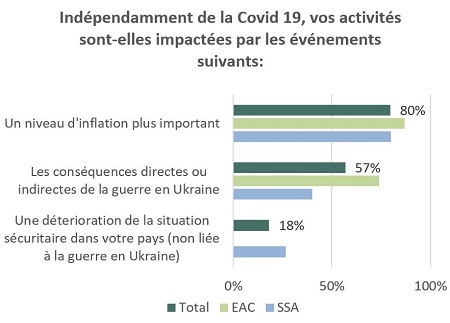

This survey clearly shows that, from now on, factors other than the COVID-19 crisis are having an impact on the activities of our partners. The first, mentioned by 80% of those surveyed, is the increase in inflation in recent months. Thus, the vast majority of the countries where the respondents operate are affected by the significant rise in energy costs and, to a lesser extent, the rise in agricultural product costs. These factors, closely linked to the outbreak of war in Ukraine, therefore have a global impact. Our partners in sub-Saharan Africa are also noting the difficulties in obtaining supplies from abroad in the current context, reinforcing fears of a food crisis.

This survey clearly shows that, from now on, factors other than the COVID-19 crisis are having an impact on the activities of our partners. The first, mentioned by 80% of those surveyed, is the increase in inflation in recent months. Thus, the vast majority of the countries where the respondents operate are affected by the significant rise in energy costs and, to a lesser extent, the rise in agricultural product costs. These factors, closely linked to the outbreak of war in Ukraine, therefore have a global impact. Our partners in sub-Saharan Africa are also noting the difficulties in obtaining supplies from abroad in the current context, reinforcing fears of a food crisis.