@Designed by pikisuperstar / Freepik

ADA, Inpulse and the Grameen Crédit Agricole Foundation have joined forces to closely monitor and analyse the effects of the COVID-19 crisis among their partners around the world. This monitoring will be carried out periodically throughout the year 2020 with the purpose of evaluating the evolution of the crisis. Through this constant and close analysis, we hope to contribute, in our own way, to the structuring of strategies and solutions tailored to the needs of our partners, as well as the dissemination and exchange of information among the different actors in the sector.

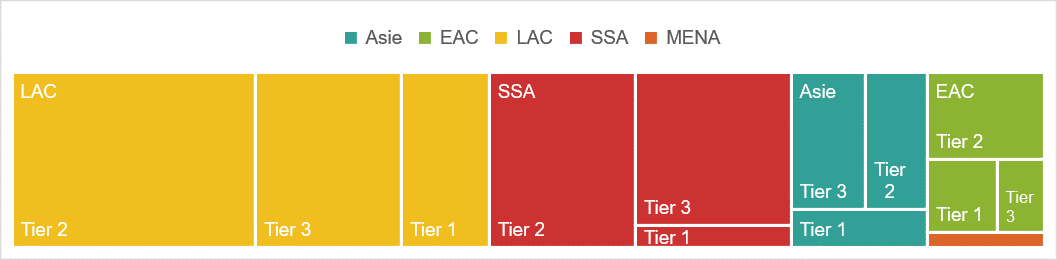

The results presented in this article come from the second wave of a joint (1)survey by ADA and Grameen Crédit Agricole Foundation, Inpulse having decided to join the initiative for odd-numbered waves. The responses were collected from 18 June to 1 July from 108 microfinance institutions (MFIs) based mainly in Latin America and the Caribbean (LAC, 46%), Sub-Saharan Africa (SSA, 29%), Asia (14%) and Eastern Europe and Central Asia (EECA, 10%), with a single MFI from the Middle East and North Africa (MENA) region. This panel of respondents spans a relatively diverse range of MFI sizes, with 49% of Tier 2 MFIs,(2) 35% of Tier 3 MFIs and 16% of Tier 1 MFIs. Figure 1 shows their regional distribution.

Figure 1. Respondents by region and tier

![]() MENA Tier 2

MENA Tier 2

In short:

The latest wave of the survey reveals that the crisis faced by MFIs has laid bare the structural strengths and weaknesses specific to their sizes: the biggest MFIs (Tier 1) appear better equipped to overcome the financial difficulties resulting from the health crisis and epidemic containment measures, as well as to take crisis management measures and make use of the specific measures put in place by local authorities. Smaller MFIs (Tiers 2 and 3), on the other hand, are more likely to offer their clients non-financial services to help them cope with the situation and are eager to continue developing non-financial services in the future. More generally, if they are considering launching new products or services, it is mainly to meet the needs of their clients rather than following their strategy or reducing risks. While big MFIs appear to be more resilient in times of crisis, small ones are also rising to the challenge and staying true to their powerful social mission. This is a real strength for these institutions, which should not be neglected in favour of more autonomous structures during the current crisis.

The biggest MFIS are less exposed to financial difficulties…

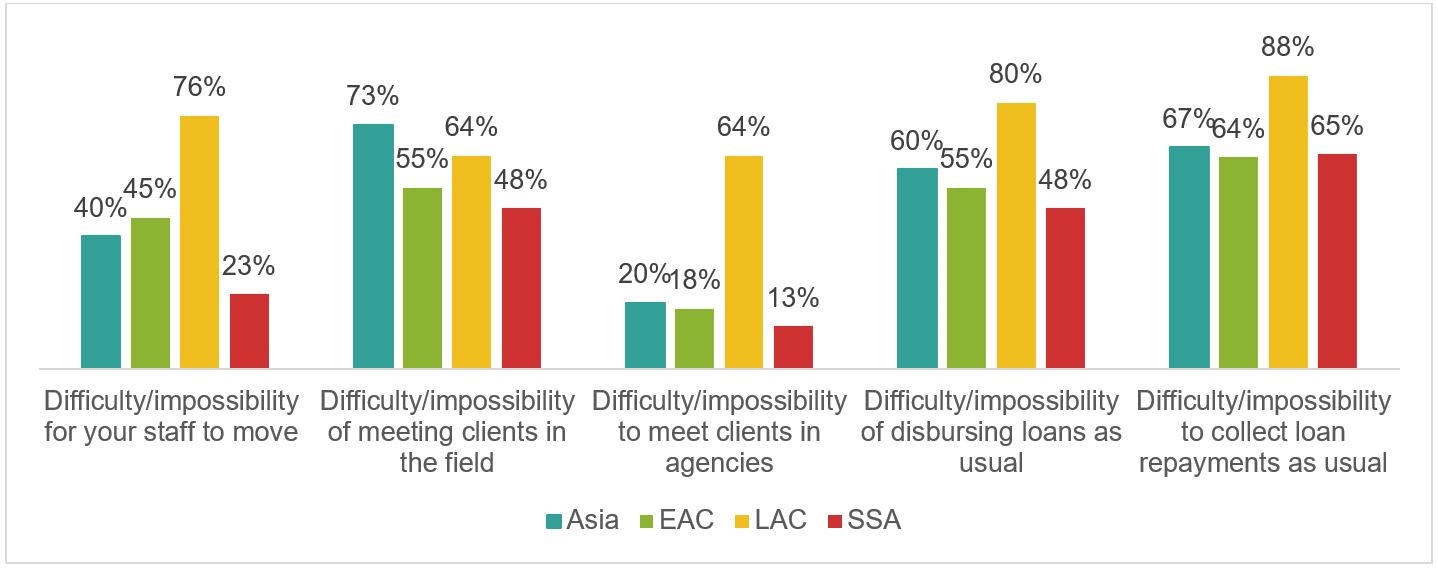

Since June, epidemic containment measures have been relaxed in certain regions, particularly Eastern Europe, Central Asia and Sub-Saharan Africa. As a result, the operational difficulties faced by microfinance institutions have ebbed in these regions since May,(3) but they are still very much present in Latin America and the Caribbean, where containment measures are still in place and a higher percentage of MFIs still find it difficult to move around, meet clients in agencies and, therefore, to disburse loans and collect loan repayments, as can be seen in Figure 2. For example: 76% of MFIs in the Latin America and the Caribbean region report that their staff is finding it difficult to move around, compared to 23% in Sub-Saharan Africa.

Figure 2. Operational difficulties faced by MFIs by region:

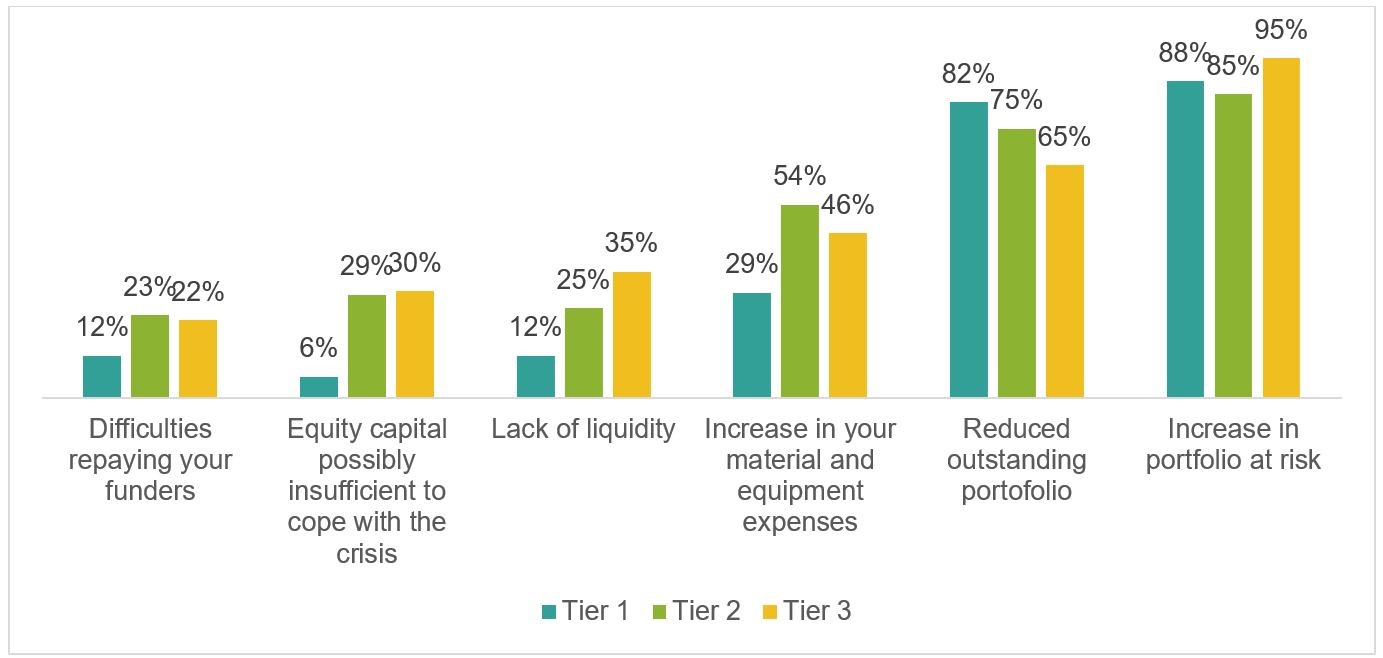

As explained in our previous article, these operational difficulties are having an impact on the portfolio and its quality in all MFIs. However, the resulting financial difficulties vary by MFI size. Overall, the biggest MFIs are less likely to face these types of problems, with lower percentages of Tier 1 MFIs reporting difficulties in repaying funders (12% versus 22.5% of Tier 2 and 3 MFIs), insufficient equity capital to cope with the crisis (6% versus 29% of Tier 2 and 3 MFIs) or lack of liquidity (2% versus an average of 29% of Tier 2 and 3 MFIs), as can be seen in Figure 3. Tier 1 MFIs appear better equipped to absorb the impact of the crisis on their financial situation.

Figure 3. Financial difficulties faced by MFIs by size

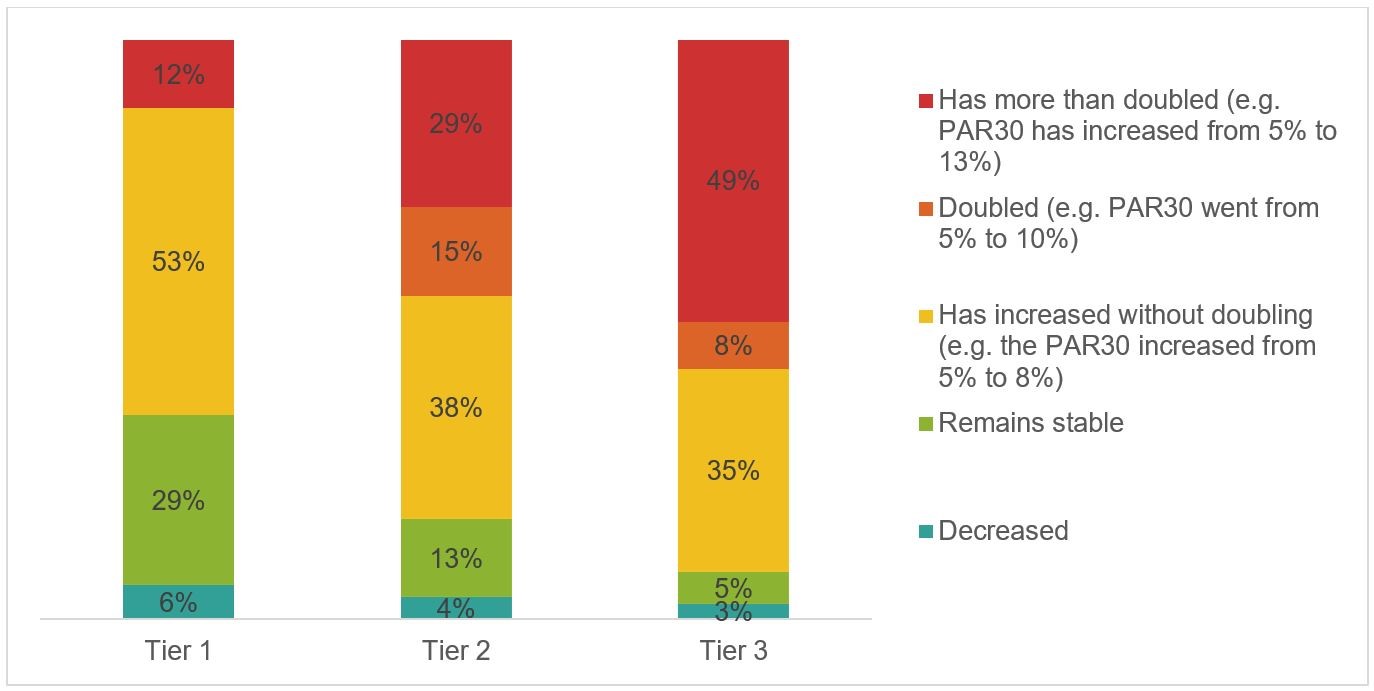

Although an increase in the portfolio at risk is the main difficulty faced by all MFIs, this increase varies by MFI size. Tier 1 MFIs have experienced smaller increases than other MFIs, as can be seen in Figure 4: only 12% of Tier 1 MFIs report that their portfolio at risk at 30 days has doubled or more than doubled compared to end 2019, versus 44% of Tier 2 MFIs and 57% of Tier 3 MFIs. In contrast, 35% of Tier 1 MFIs report a stabilisation or decrease in this indicator, versus 17% of Tier 2 MFIs and 8% of Tier 3 MFI.

Figure 4. Changes in the PAR30 of MFIs compared to end 2019 by MFI size

…and more likely to implement crisis management solutions…

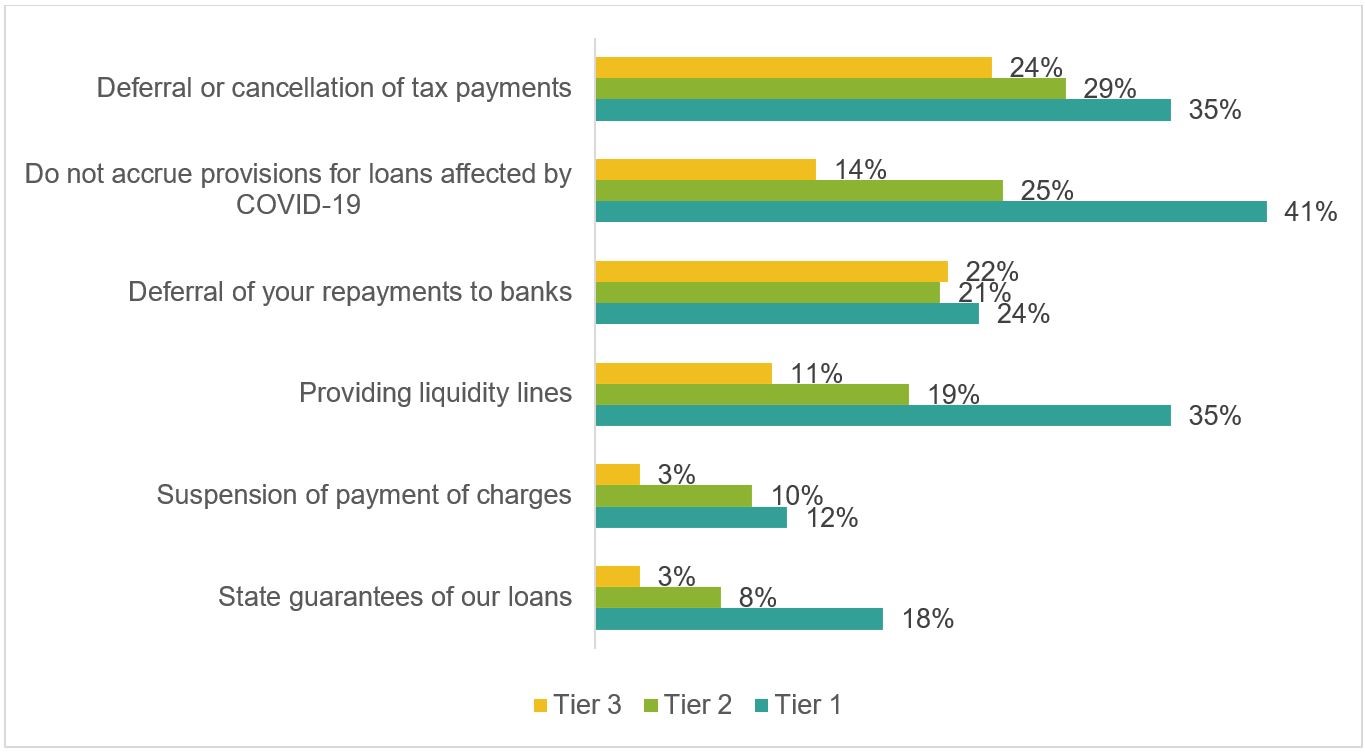

The governments of most countries have taken measures to help microfinance institutions to weather the crisis. However, not all MFIs are benefiting from these measures. While the exact percentages vary from one region to the next, probably due to differences in the communication and implementation of these measures (e.g. MFIs in Asia are more likely to report making use of a certain number of measures), geographic location does not appear to be the sole determining factor for making use of certain government measures: bigger MFIs are also more likely to benefit from them, as can be seen in Figure 5.

Figure 5. Government measures from which MFIs have benefited by MFI size

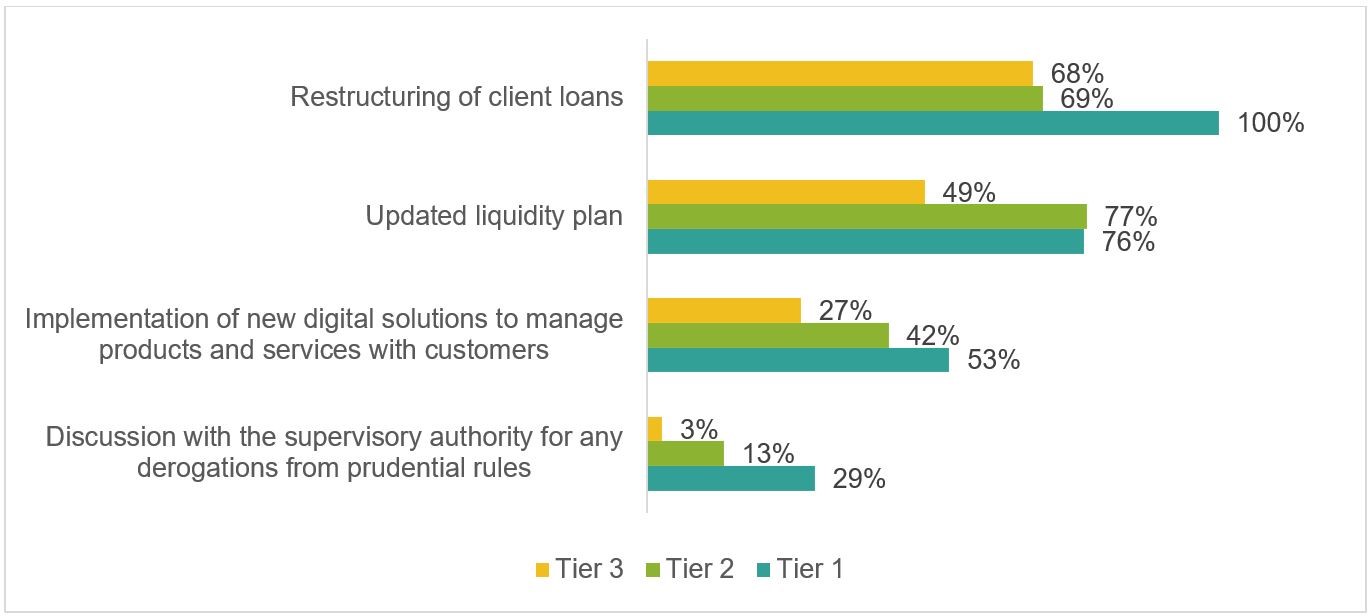

This size effect is real because it cannot be explained by a specific distribution of MFIs by region. For example, when it comes to rescheduling or cancelling the payment of taxes and the non-provision of loans affected by COVID-19, a regional analysis shows that MFIs in Asia are more likely to benefit from these measures despite Tier 1 MFIs being in the minority in this region. Similarly, when it comes to liquidity lines, MFIs in Sub-Saharan Africa are among the most likely to benefit from them despite Tier 1 MFIs being few and far between in this region. As for the operational and crisis management measures implemented, the types of measures again vary by MFI size (Figure 6): For example, 100% of Tier 1 MFIs in the sample restructured client loans, versus an average of 69% of other MFIs. They are also more likely to engage with supervisory authorities to explore the possibility of suspending prudential regulations during the crisis. In contrast, Tier 3 MFIs are less likely to use their liquidity plans or implement new digital solutions.

Figure 6. Operational and crisis management measures taken by MFIs by size

…while small MFIS continue to focus on their clients’ needs

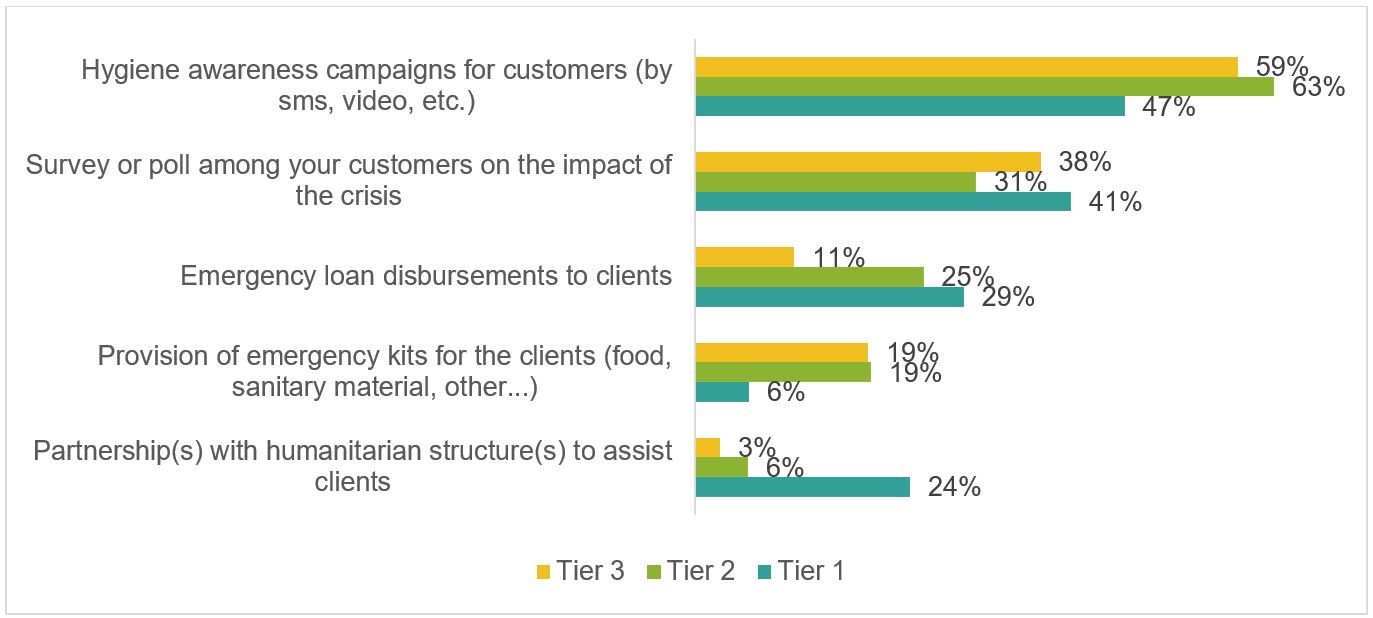

In contrast, despite facing significant challenges, the smallest MFIs continue to focus on their clients’ needs: for example, they are more likely than Tier 1 MFIs to have surveyed their clients to better understand the impact of the crisis (Figure 7). On the other hand, although they were less likely to disburse emergency loans to their clients, they were more likely to implement measures that went beyond their core business to better meet the needs of their clients during the health crisis. For example, more of these MFIs launched hygiene awareness campaigns on hygiene or provided clients with emergency kits. Bigger MFIs were less likely to offer these types of direct services to clients, instead forging partnerships with specialised

organisations.

Figure 7. Crisis response measures for clients by MFI size

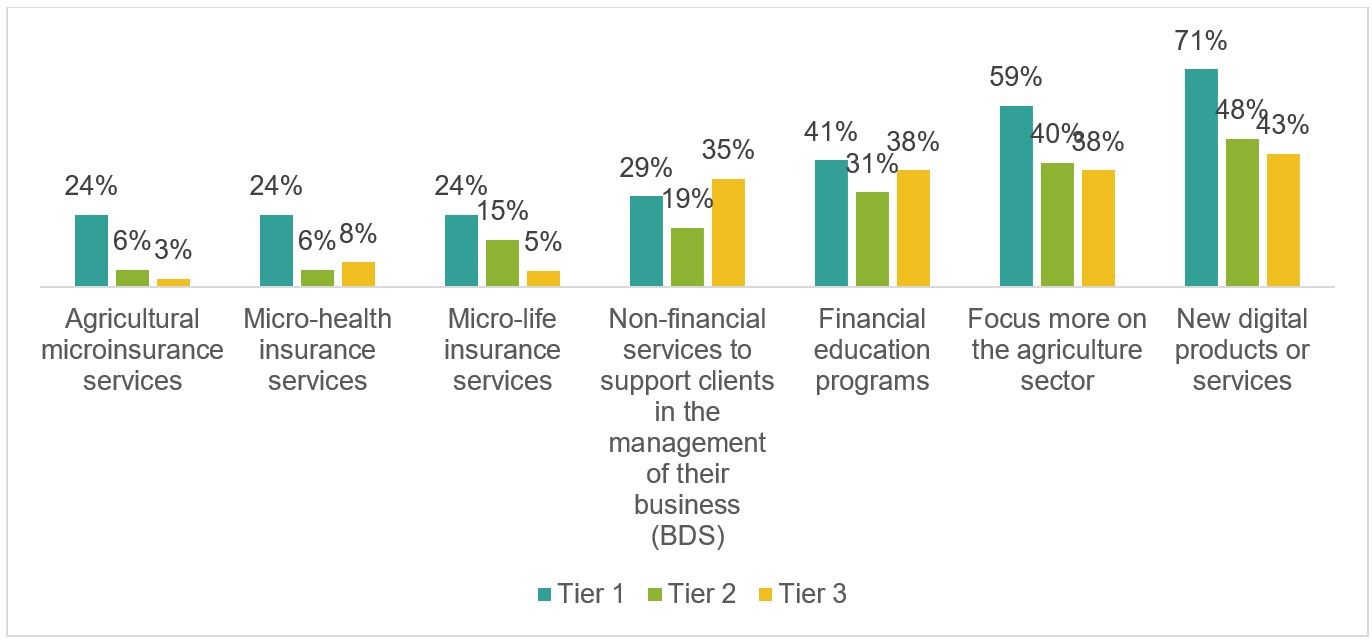

More Tier 1 MFIs reported interest in launching new products or services in the medium term; as shown above, these MFIs have fewer financial constraints and, therefore, more room for manoeuvre in this regard (Figure 8). More specifically, while few MFIs overall are planning to launch microinsurance products in the future, Tier 1 MFIs are the most likely to do so. They are also more likely to want to increase their focus on agriculture or launch new digital products and services. The smallest MFIs, on the other hand, also want to start offering non-financial services such as financial literacy and business development services.

Figure 8. New products, services or markets that MFIs wish to develop in the medium term, by size

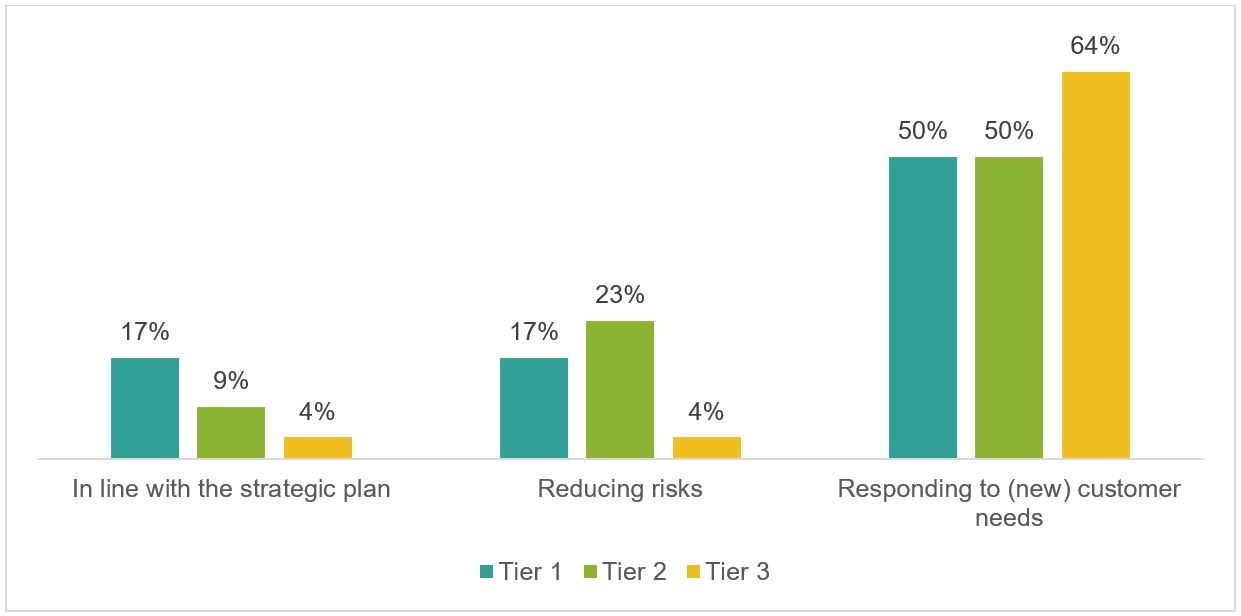

The motivations for MFIs to focus on new markets or develop new products or services also vary by size (Figure 9): Among those that reported wanting to launch at least one new product or service and stated their motivations (76 out of 108 respondents), the desire to meet the new needs of clients and/or follow new market trends was more frequent among Tier 3 MFIs than among MFIs in other tiers. In contrast, there are fewer that base this choice on following their strategic plan or striving to reduce risks. The focus of the smallest MFIs on their clients’ needs will probably become one of their strong points during this crisis.

Figure 9. Main motivations for MFIs to focus on new markets, products or services by size

_____________________________________________________________________________

_____________________________________________________________________________