ADA, Inpulse and the Grameen Crédit Agricole Foundation have joined forces to closely monitor and analyze the effects of the COVID-19 crisis among their partners around the world. This monitoring will be carried out periodically throughout the year 2020 with the purpose of evaluating the evolution of the crisis. Through this regular and close analysis, we hope to contribute, in our own way, to the structuring of strategies and solutions tailored to the needs of our partners, as well as the dissemination and exchange of information among the different actors in the sector.(1)

In short

This article is based on the answers provided between July 23rd and August 6th 2020 by 91 partners located in 42 countries, split between Europe, Africa, Asia and Latin America (2). Feedback from these microfinance institutions (MFIs) allows us to observe the continuous evolution of the sanitary crisis linked to the COVID-19 virus. While the measures to reopen borders and to revive the economy have multiplied during the month of July, our partners mention significantly that the virus now directly affects their customers and employees.

In such an uncertain and evolving context, MFIs have been braving the challenges they face for more than a quarter now. With operational difficulties still ongoing, institutions remain vigilant about their portfolios and the risk they carry, which seems to have stabilized overall, albeit at a much higher level than before the crisis. Nevertheless, some signals are encouraging on other issues. For example, the vast majority of MFIs believe that they can survive the crisis without major strategic changes. In addition, it appears that the issue of liquidity has been rather well managed since the beginning of the crisis.

However, the battle against the virus is not won, and its repercussions are particularly strong on the informal sector of the economy. It appears that clients in the informal economy are more affected, particularly as they do not ultimately benefit from the aid measures that states can provide. Nonetheless, MFIs are sensitive to these needs and some of our partners are considering providing specific services to help their clients cope with the crisis.

1. Operational constraints remain relevant for MFIs

1. Operational constraints remain relevant for MFIs

1. Operational constraints remain relevant for MFIs

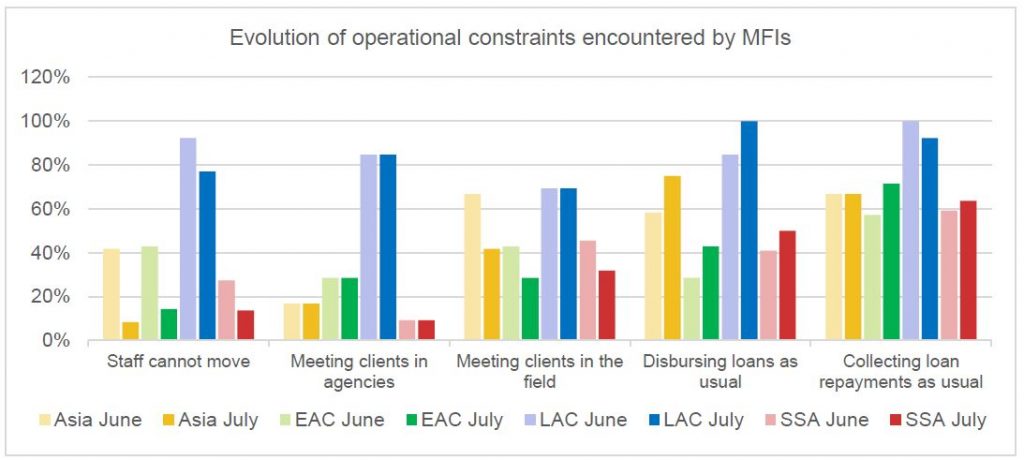

1. Operational constraints remain relevant for MFIsIn general, our partners are reporting progress regarding the easing of containment measures in their countries, following the first relaxations that took place in some regions of the world in June (notably in Eastern Europe, Central Asia and Sub-Saharan Africa). Comparing the responses of our partners who answered to our July and June surveys (3) (graph below) reflects the improvement of operational difficulties. Moreover, these figures are in line with the general results obtained for the month of July.

MFIs in each region report an improvement in travel opportunities for their staff. However, this remains a major constraint in Latin America and the Caribbean, while less than 20% of MFIs in other areas are affected by this issue. Moreover, even if mobility is improving, meeting clients in the field remains an important issue for more than 30% of MFIs. Finally, with the exception of Latin America, meeting clients in branches seems to be the least problematic solution today.

In fact, while there has been an overall enhancement in interaction with clients in all regions, collecting loan repayments or disbursing new loans at standard pre-crisis levels remains very difficult, with such challenges being encountered by more than 50% of the MFIs surveyed in each region (70% and 66% respectively overall). Such difficulties are ultimately linked to national or local regulatory constraints.

“Though other MFIs start operating their process, we still wait for full release by the regional government” – Partner in Myanmar

Especially as MFIs are still busy restructuring client loans in July (80% of respondents).

“Communication on the postponement of instalments is a barrier to the repayment of loans” – Partner in Senegal

Although we have been observing the singularity of the Latin American zone in the responses collected over the last few months due to a particularly difficult COVID-19 sanitary context, the information we gathered shows that the situation is not settled yet in the other regions.

Although we have been observing the singularity of the Latin American zone in the responses collected over the last few months due to a particularly difficult COVID-19 sanitary context, the information we gathered shows that the situation is not settled yet in the other regions.

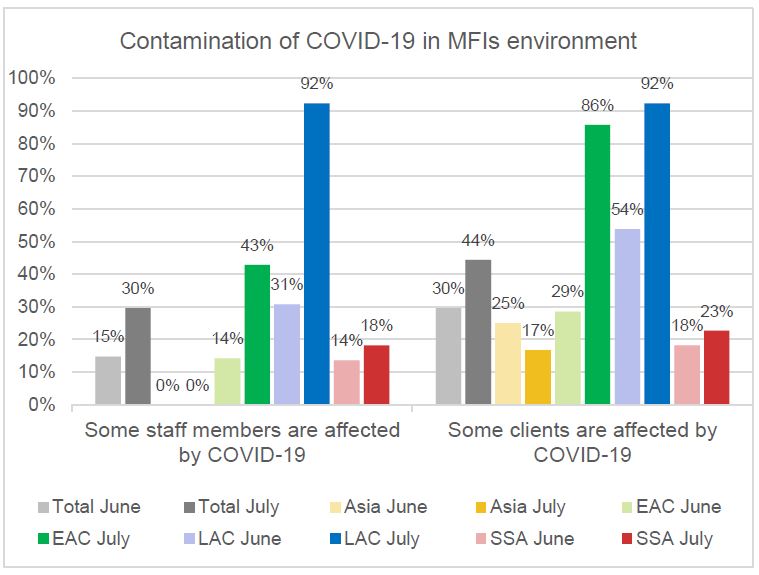

In fact, doubts about a potential normalization of MFIs’ activities have not been dispelled for now, as the health crisis remains the central issue of the current period and as it persists. The news in July were notably highlighted by the punctual resurgence of a number of cases in some countries. For the first time in our surveys, this is significantly demonstrated by a sharp increase in the proportion of partners who are affected by the health crisis, both among their staff and their clients (see graph below (4)).

Thus, at the global level of the survey, 51% of our partners told us that among their customers, some have contracted COVID-19. Almost a third indicate that this also concerns their employees. Although we do not have data to know the respective proportions of customers and employees concerned, this trend is still meaningful. More specifically, more than three out of four MFIs in Central Asia and Latin America reported having clients infected with the virus (one out of two in June). While Latin America is largely affected on both the client and staff sides, the figures are also slightly higher for the staff of MFIs in Europe and Central Asia. South Asia and Sub-Saharan Africa seem to be generally less affected on this point, but figures encourage us to remain vigilant.

“More than 10 clients have died from Covid-19” – Partner in Honduras

2. MFIs continue to face major financial issues

2. MFIs continue to face major financial issues

2. MFIs continue to face major financial issues

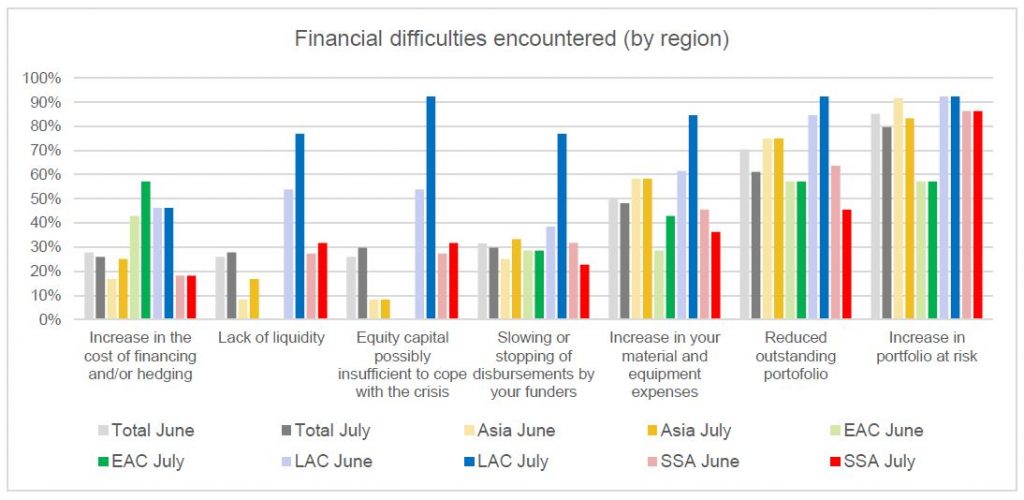

2. MFIs continue to face major financial issuesAs we witnessed since the beginning of our surveys, the increase in portfolio at risk and the reduction in outstanding portfolio are the two main direct consequences of the crisis for a microfinance institution. Other financial difficulties are to a lesser extent and are stable from June to July (figure below5). This is the case in all regions except Central America, where our partners who responded to all of our surveys indicate problems and growing fears regarding equity, lack of liquidity or increased expenses.

The details of the analysis show that the contraction of the credit portfolio is a heterogeneous phenomenon. Among all respondents, 39% of Central Asian MFIs indicate that they are suffering from a reduction in their portfolio, compared to 55% in Sub-Saharan Africa, 71% in South Asia and 88% in Latin America during the same period.

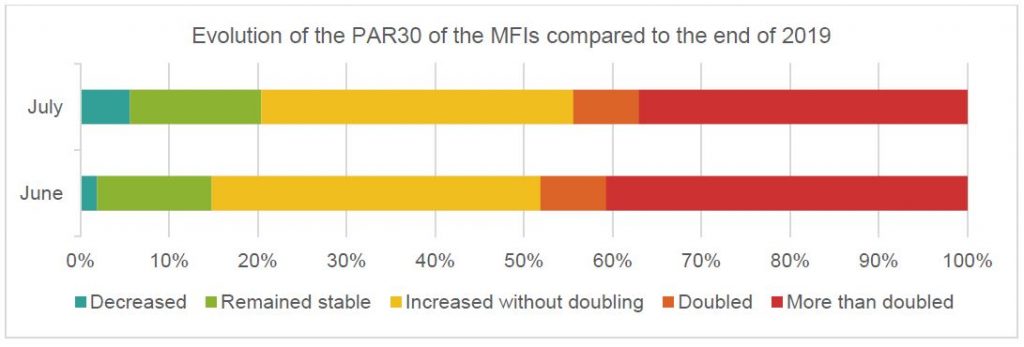

On the  other hand, it appears that the increase in portfolio at risk is a common problem for all MFIs, regardless of their region or size, and concerns more than 80% of our partners. However, if the PAR 30 of microfinance institutions has deteriorated since the beginning of the crisis, it is no longer undergoing major changes between June and July, although it remains at a much higher level than before the crisis. As shown in the graph below, the PAR30 structure of the partners in the sample of 54 MFIs is stable from one month to the other. Moreover, we observe this trend across all of the surveyed MFIs: between 15 and 20% of the MFIs see their PAR30 decreasing or remaining stable, while around 40% have seen their PAR30 increase without doubling since the end of 2019. Finally, the riskiest cases represent between 30 and 40% of the respondents.

other hand, it appears that the increase in portfolio at risk is a common problem for all MFIs, regardless of their region or size, and concerns more than 80% of our partners. However, if the PAR 30 of microfinance institutions has deteriorated since the beginning of the crisis, it is no longer undergoing major changes between June and July, although it remains at a much higher level than before the crisis. As shown in the graph below, the PAR30 structure of the partners in the sample of 54 MFIs is stable from one month to the other. Moreover, we observe this trend across all of the surveyed MFIs: between 15 and 20% of the MFIs see their PAR30 decreasing or remaining stable, while around 40% have seen their PAR30 increase without doubling since the end of 2019. Finally, the riskiest cases represent between 30 and 40% of the respondents.

“[It is difficult] to cover the expenses of provisions for doubtful debts” – Partner in the Democratic Republic of Congo

Luckily, all these difficulties should not be too harsh for our partners. When asked about possible strategic changes because of the crisis, 93% of respondents do not anticipate any changes in the short or medium term. Therefore, our partners do not feel concerned by potential sales of a part of their assets, being placed under administrative supervision or being liquidated, which is a sign of a certain confidence in the future.

Luckily, all these difficulties should not be too harsh for our partners. When asked about possible strategic changes because of the crisis, 93% of respondents do not anticipate any changes in the short or medium term. Therefore, our partners do not feel concerned by potential sales of a part of their assets, being placed under administrative supervision or being liquidated, which is a sign of a certain confidence in the future.

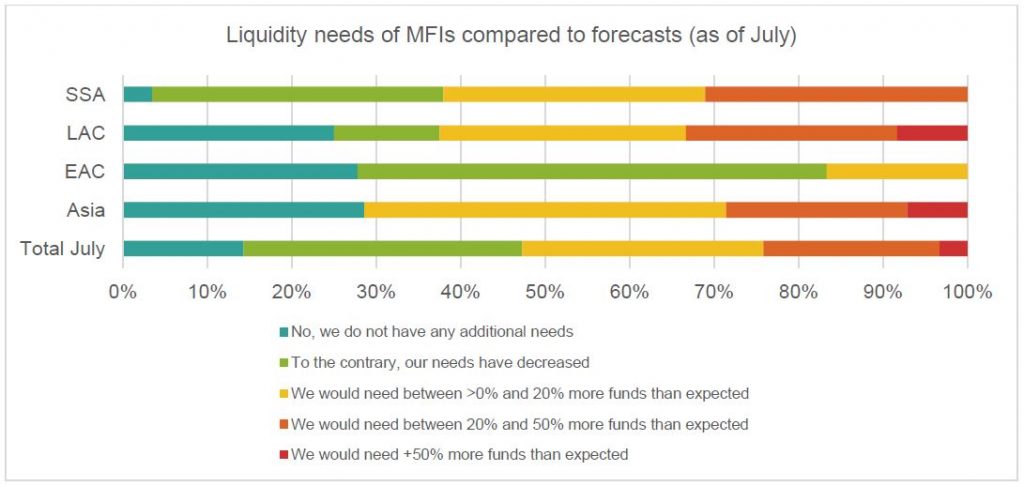

Finally, the latest information from our partners indicates that a liquidity crisis seems to have been avoided, with 24% of respondents highlighting this problem (compared to almost 40% in our May survey). In details, the proportion of MFIs raising this point in each region does not exceed one third.

The first explanations lead us to the many extensions of maturities granted to MFIs by their foreign and local investors, but also to the reduced levels of disbursements since the beginning of the crisis. We also note the low proportion of MFIs that have suffered from significant withdrawals of savings, which has helped cash management. Among the MFIs reporting this difficulty, most are from Sub-Saharan Africa and Asia and do not show significant additional liquidity needs compared to other MFIs. These different factors influence the liquidity needs of MFIs. Thus, on a global scale, 47% of the respondents have no additional funding needs for 2020. For almost a quarter of the MFIs outside Sub-Saharan Africa, these needs even decreased. Last, only 25% of those surveyed report significant additional needs.

3. In July, the informal sector is exposed

3. In July, the informal sector is exposed

3. In July, the informal sector is exposed

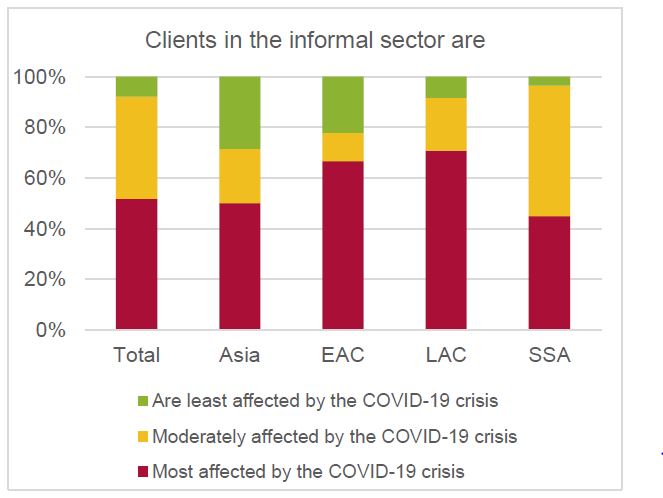

3. In July, the informal sector is exposedMicrofinance institutions are still exposed to the crisis, and so are their clients. In fact, 92% of our partners indicate that clients in the informal economy are either moderately affected by the crisis or are the most affected ones. Like all other entrepreneurs and clients of MFIs, they face reduced activity, but also suffer from the consequences of the major international and national measures to manage the pandemic, for instance in the tourism, textile or cultural sectors… With limited means of relief and a reduced activity that cannot generate sufficient income, they would be more vulnerable. This point is raised overwhelmingly in Central Asia and Latin America (two thirds of respondents from these regions) while in Sub-Saharan Africa, the feedbacks indicate that clients in the informal economy are affected in the same way than those in the formal economy.

“Due to prevailing market and economic conditions, it is hard for the small businesses to revive their usual economic activities to the level they were before COVID-19 crisis” – Partner in Sri Lanka

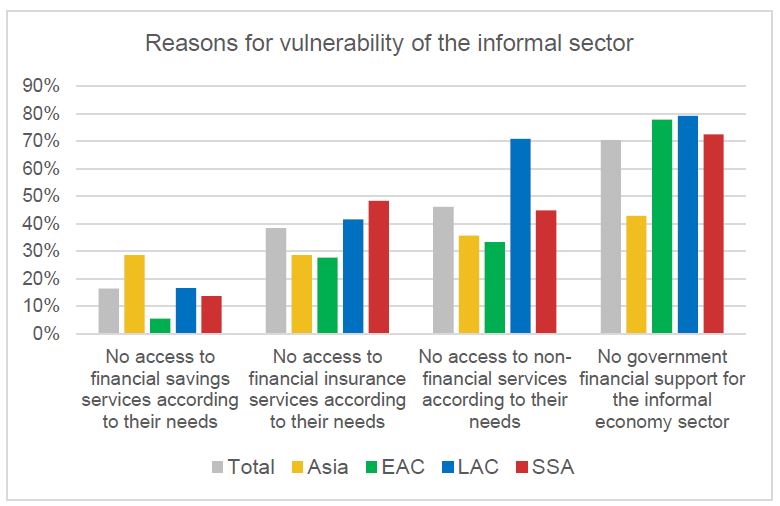

The reasons given by our partners are mostly about financial matters: the vulnerability of workers in the informal sector would come from the lack of financial support from governments to the sector. This explanation is given by a vast majority of surveyed MFIs (78%), which also note (57%) that clients in this sector do not have access to adapted non-financial services (business development, financial education, health education, etc. ). The lack of insurance services is also underlined by 50% of MFIs. In contrast, the lack of access to savings services is hardly mentioned.

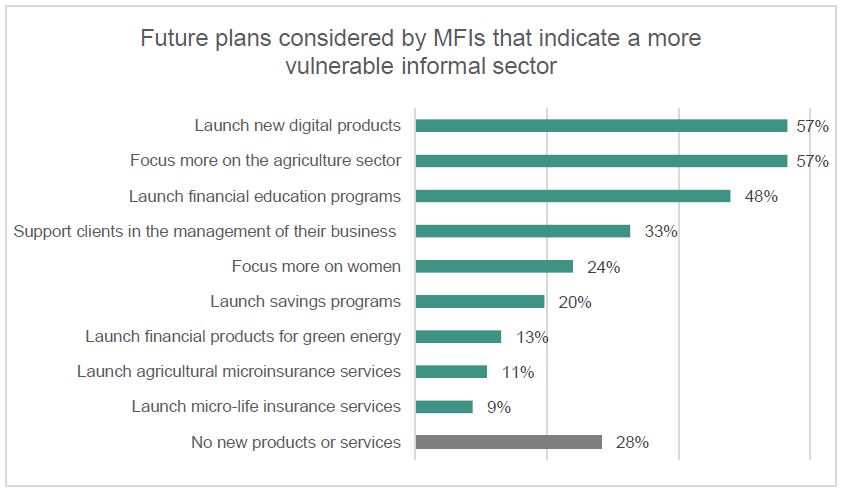

MFIs are already thinking about how to meet the needs of their clients. Thus, 48% of MFIs reporting a vulnerable informal sector say they plan to launch financial education programs, and 33% imagine supporting clients in the management of their activity. However, only a small proportion of them forecasts launching micro insurance products (maximum 11%). MFIs justify such motivations with two main reasons: getting closer and focusing on under-served populations, but also to respond to a demand for adapted offers during a particular period. For some MFIs, this could translate into other initiatives, such as the development of the agricultural segment (still strongly mentioned by MFIs) or by the development of digital solutions for clients. As a partner in Latin America tells us:

“The financial education and business management program is being planned by digital means to introduce customers to the use of social networks to sell their products, since the main problem they have had is that their places of sale have been closed down or customers are not arriving because of the risk of contagion”

The results of this article highlight the operational and financial difficulties encountered by MFIs during this first semester, but also their first steps in understanding the problems and finding solutions. In this context, the future challenges us to continue questioning ourselves about the best recovery actions for each region, how they can be implemented and how the various actors in the microfinance sector can directly and indirectly contribute to its revival.

_____________________________________________________________________________

1 The results of the previous surveys are available here for the first one and here for the second one.

2 The total number of MFIs that responded to the survey for each region is as follows: South Asia (“Asia”) 14, Latin America and the Caribbean (“LAC”): 24, Europe and Central Asia (“ECA”): 18, MENA: 6, and Sub-Saharan Africa (“SSA”) 29 (total: 91 institutions). The small sample from the MENA region does not allow for the monitoring of the figures for the zone.

3 This comparison is based on a sample of 54 MFIs: 12 in Asia, 7 in EAC, 13 in LAC, 22 in SSA.

4 This comparison is also based on the sample of 54 MFIs.

5 This comparison is also based on the sample of 54 MFIs.