“The need to act in the face of environmental risks is a logical consequence of the mission our institution has set for itself: to help the most vulnerable populations.”

Microfinance sector stakeholders, historically organized to promote access to financing for vulnerable populations, must evolve their tools and intervention methods in a context of climate and environmental emergency that can no longer be ignored. Rural populations, living in economically fragile areas, are indeed highly exposed to these effects due to their dependence on agriculture and their difficulties in accessing basic services (access to water, energy, acceptable sanitary conditions, etc.).

To better understand these mechanisms, we conducted a series of qualitative interviews with microfinance institutions that are partners of the Grameen Crédit Agricole Foundation, which supplemented questionnaires that have been regularly sent and analyzed for several months. This approach allowed us to identify the main environmental risks faced by these institutions and the means implemented to prevent and address them. Here, we share some of our analysis and the avenues of reflection that our partners have already initiated.

1. Weather risks are the most urgent to address

Weather-related natural disasters and disruptions to the seasonal cycle are increasingly impacting the activities of MFI clients. For 65% of our partners, weather risks will constitute the most significant environmental threat in the near future. Vulnerable and rural populations in particular are more exposed due to their dependence on agriculture, the fragility of their infrastructure, and their difficulties accessing healthcare. Our partner institutions share numerous examples of disruptions that impact their clients' activities. Droughts affect yields and reduce access to drinking water, and floods destroy crops and infrastructure and interrupt supply chains.

The extent and nature of environmental risks vary greatly depending on the region. Sub-Saharan Africa is the geographic area where our partners suffer the most from weather risks: it has already materialized in 40% of them. Significant risks of erosion and soil pollution are also reported in this region more than elsewhere. However, health risks linked to air pollution are more of a concern for our partners in Eastern Europe and Southeast Asia.

2. Strong awareness, but implementation still insignificant

Our partners are widely aware of the environmental risks that affect their activities. The vast majority, 88% of respondents, consider protecting their beneficiaries against environmental risks to be part of their mission. However, this does not necessarily translate into concrete actions at this time. The commitment of the institution's governance appears to be an essential prerequisite: many institutions indicate that decisions in this regard are only made and implemented when governance is truly involved in monitoring environmental issues. Among the 88% of respondents who believe that environmental aspects are included in their mission, 16% do not yet have any tangible involvement of their governance in these matters.

3. Institutions are not yet sufficiently proactive on environmental issues

One of the levers for encouraging institutional governance to take action is client demand: many institutions have observed that when clients express their expectations for specific services or financing related to the climate transition (irrigation equipment, adapted seeds, access to energy, etc.), boards of directors are more inclined to want to develop new offerings and to ask their teams for greater involvement on this topic. However, only 40% of our partner MFIs observe explicit requests from their clients on these environmental issues, which suggests real potential on this point.

The influence that donors can also exert reinforces this institutional commitment. Among our most advanced partners on these issues, many have been encouraged or supported by their own financiers to define an environmental strategy or design inclusive green finance products. This is the case for four of the seven partners of the Grameen Crédit Agricole Foundation with whom we conducted qualitative interviews.

4. Inspiring initiatives have already been implemented by certain institutions

Several of our partners have already implemented interesting initiatives to strengthen the resilience of their activities in the face of environmental risks and limit the portfolio's contribution to these risks.

To protect clients and thus their business, 51% of our partner institutions raise awareness among their clients about the vulnerability of their business to the effects of climate change (declining yields, impact of weather hazards, etc.). 35% of them have exclusion lists, which prohibit the financing of practices that weaken clients' businesses, such as the use of pesticides or over-farming, which pollute and impoverish the soil. A third of our partner MFIs train their clients in more resilient practices, particularly in the agricultural sector. Finally, one of the most common actions is that dedicated to promoting the creation of precautionary savings, proposed by 25% of the institutions. It allows small producers to provide for and anticipate potential climatic hazards (drought, floods, cyclones, etc.).

Another effective way to protect customers is to offer specific insurance products, particularly agricultural insurance, but these are often difficult and complex to implement. A smaller number offer emergency loans and loans with flexible conditions precedent to quickly meet customer needs in the event of a natural disaster.

To limit the contribution of client activities to environmental risks, 65% of our partners have adopted what could be considered "sector-specific policies." These policies exclude activities that promote deforestation, water or air pollution, or waste generation. More than 50% of our partners raise awareness among their clients about the impact of their activities, such as excessive water or energy consumption. 51% of the MFIs surveyed finance low-consumption equipment or clean energy transitions. This includes, for example, low-energy cooking methods, solar equipment, and home insulation. Finally, 47% finance environmentally friendly agricultural and livestock practices. This financing often complements client training and awareness-raising initiatives to strengthen agricultural value chains.

5. MFIs encounter numerous obstacles in implementing their environmental offerings

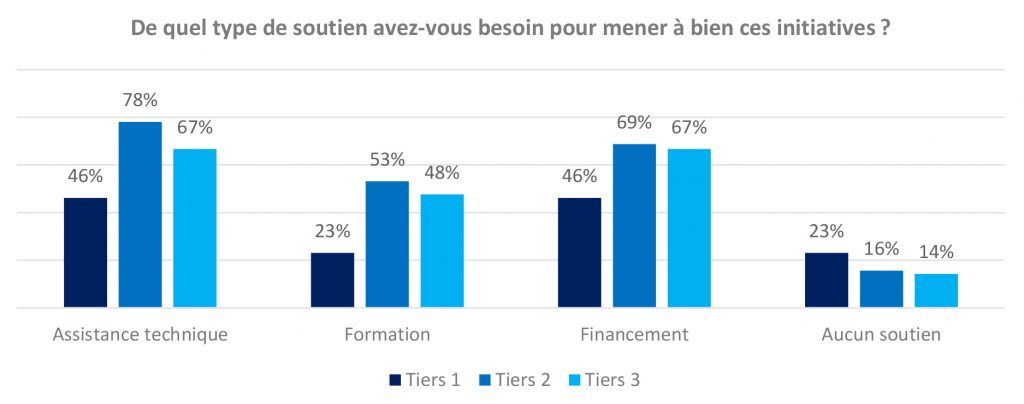

While we are able to provide numerous examples of initiatives from our partner institutions, these still concern a limited number of them. Although 64% of the institutions that responded to our survey have future projects on these themes, they face financial and technical obstacles: 78% of them state that they lack the financial resources and 52% the expertise to implement their projects. In terms of financial support, MFIs are seeking financing lines of more than 3 years, as well as loans at favorable rates indexed to environmental performance objectives. Technical assistance is also an effective tool to support companies in designing new products, raising awareness and training their clients, and adapting their activities towards greater resilience and respect for the environment. According to our interviews, receiving technical assistance plays a key role in their development, and MFIs have significant needs for technical assistance. In particular, many of our partners are interested in developing an agricultural micro-insurance offering, which requires significant resources and specific knowledge.

6. In conclusion

To advance the microfinance sector on environmental issues, it appears necessary to mobilize the governance bodies of microfinance institutions. Beyond the support offered by donors, which needs to be strengthened, this mobilization can be brought about by deepening and replicating existing effective practices on a large scale, sharing experiences between institutions, organizing forums and think tanks, and designing appropriate financial products such as microinsurance or financing agricultural value chains.

An "environmental protection pathway" remains to be built together with our peers and partners (similar to SPTF-CERISE's customer protection pathway) by building on existing initiatives in the sector (Green Index, ALINUS). The practice of "green loans," whose use is rapidly accelerating in other sectors, should be further promoted in microfinance. This involves, for example, offering preferential rates indexed to environmental performance objectives.

Technical assistance is essential to enable institutions to implement concrete actions. The need to adapt the offer to the needs of institutions is one of the main lessons learned from the in-depth evaluation of " Our technical assistance system ". As far as the Grameen Crédit Agricole Foundation is concerned, the need for adaptation applies particularly to missions on environmental themes: the environmental risks that weigh on the activities of partners vary greatly from one region to another, and even from one MFI to another. It is therefore a question of designing a technical assistance support system that is flexible and adaptable according to the specificities of the institutions and the economic situation, without imposing overly specific themes and standardized methodologies. This must be accompanied by a wide variety of possible financing for various types of technical assistance missions. Another lesson listed in the publication is the need to reflect on models for measuring the impact of missions around environmental issues, with the formulation of precise objectives and indicators.

To define relevant common indicators, both in terms of direct and indirect impact through portfolio activity, it is necessary to collectively agree on good practices and common definitions. In particular, the sector can reflect on supporting and developing more sustainable agriculture, which is undoubtedly one of the major challenges facing the most fragile countries on the African continent.

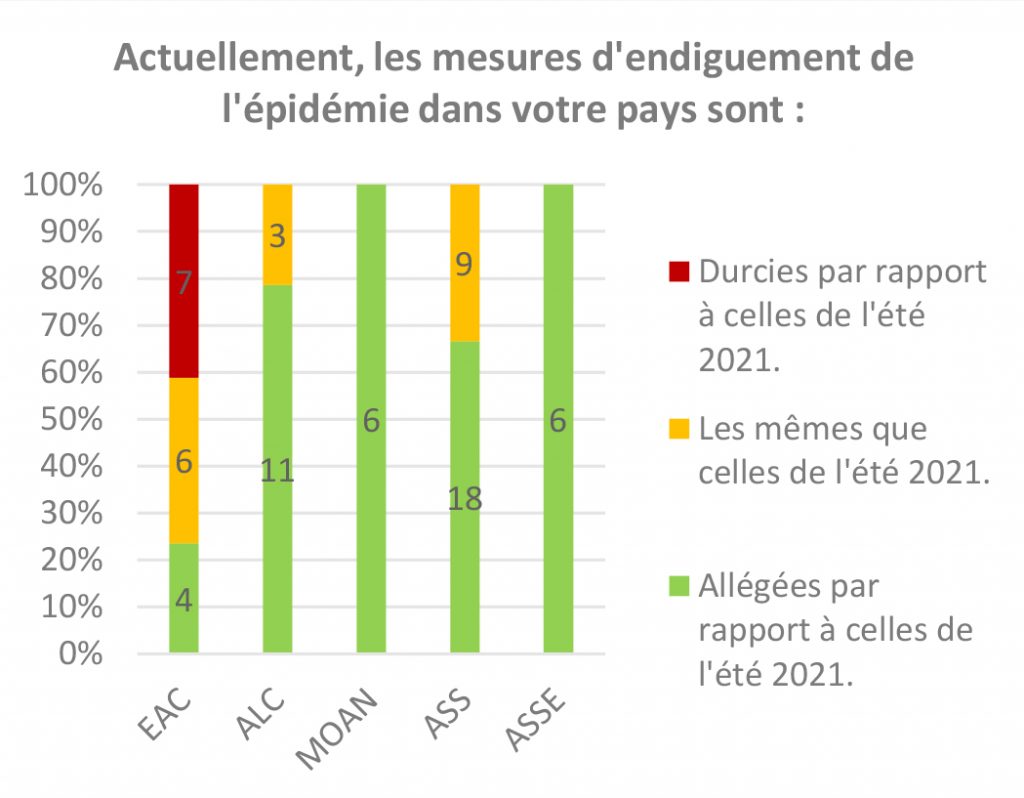

Eastern European MFIs (Bulgaria, Lithuania, Moldova, and Romania) stand out as an exception to this dynamic, as some of them (7 out of 13 MFIs in this sub-region) are experiencing a more difficult context during this period, linked to the resurgence of the epidemic in the region in the last quarter. This is reflected in particular by difficulties in meeting clients in the field or in branches and therefore in carrying out activities in general (collection and disbursement of loans).

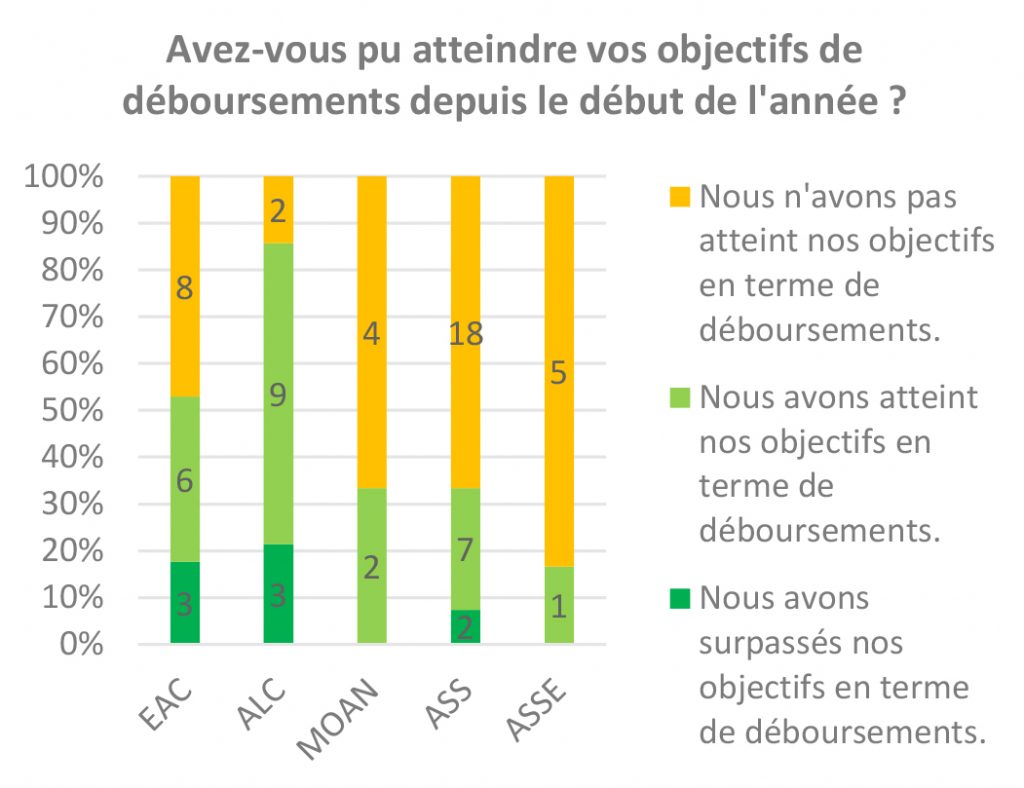

Eastern European MFIs (Bulgaria, Lithuania, Moldova, and Romania) stand out as an exception to this dynamic, as some of them (7 out of 13 MFIs in this sub-region) are experiencing a more difficult context during this period, linked to the resurgence of the epidemic in the region in the last quarter. This is reflected in particular by difficulties in meeting clients in the field or in branches and therefore in carrying out activities in general (collection and disbursement of loans). The low disbursement levels are primarily linked to the difficulties experienced by MFI clients. Among the MFIs that are not achieving the expected growth levels this year, the two most cited reasons (54% and 49% respectively) are the deteriorated risk profile of the clientele and the reluctance of clients to take out new loans. This justification is also confirmed by the fact that 53% of the respondents still have a higher-risk portfolio than before the crisis. This persistent increase in risk and the situation of a portion of MFI clients whose needs are low or even nonexistent, therefore limits the development possibilities of MFIs.

The low disbursement levels are primarily linked to the difficulties experienced by MFI clients. Among the MFIs that are not achieving the expected growth levels this year, the two most cited reasons (54% and 49% respectively) are the deteriorated risk profile of the clientele and the reluctance of clients to take out new loans. This justification is also confirmed by the fact that 53% of the respondents still have a higher-risk portfolio than before the crisis. This persistent increase in risk and the situation of a portion of MFI clients whose needs are low or even nonexistent, therefore limits the development possibilities of MFIs.

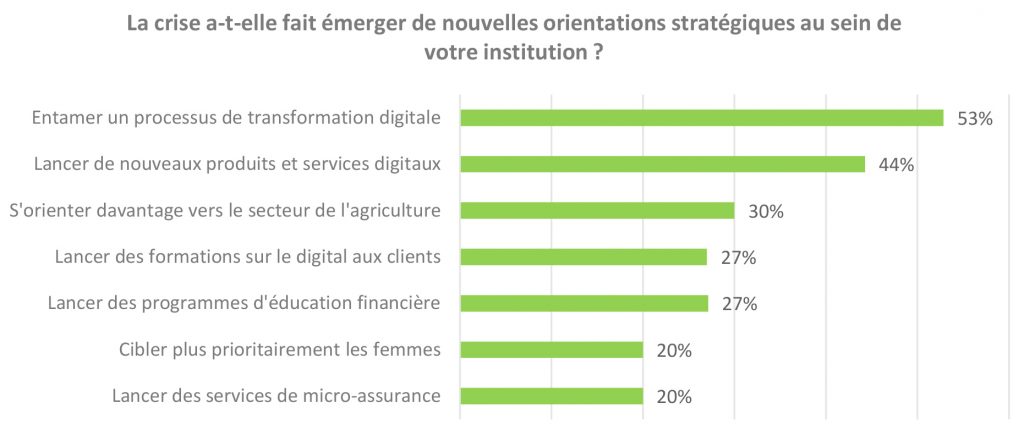

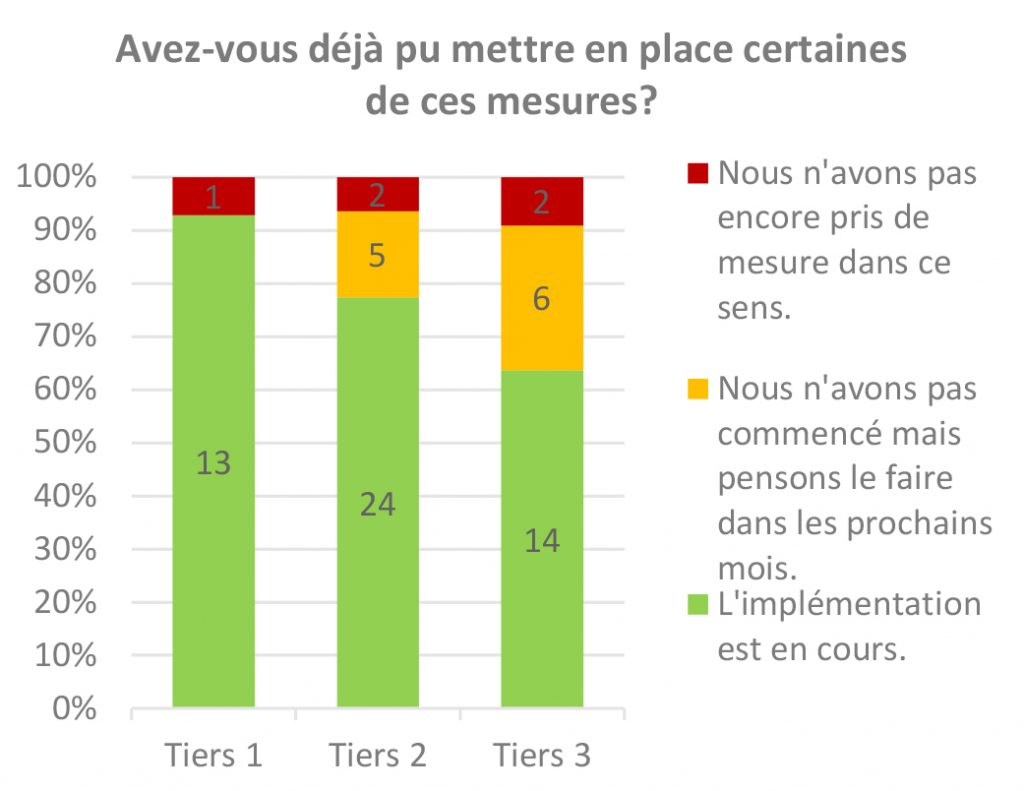

We note that 76% of the MFIs have already started implementing measures related to these strategic axes and 16% plan to launch actions in this direction in the coming months. Thus, only 7% of the sample presents less obvious prospects on this point. A certain gap in the implementation of these measures emerges, however, depending on the size of the institutions: the vast majority of Tier 1 MFIs (93%) have already implemented such measures while this proportion drops to 77% for Tier 2 and 64% for Tier 3 MFIs.

We note that 76% of the MFIs have already started implementing measures related to these strategic axes and 16% plan to launch actions in this direction in the coming months. Thus, only 7% of the sample presents less obvious prospects on this point. A certain gap in the implementation of these measures emerges, however, depending on the size of the institutions: the vast majority of Tier 1 MFIs (93%) have already implemented such measures while this proportion drops to 77% for Tier 2 and 64% for Tier 3 MFIs.